Application of Current Accounting Standards to Crypto & Digital Currency Transactions

Feb 26th, 2018 9:34 AM

This article is made available to you at no cost but requires proper credit. Mr. Cameron-Huff is also available for interviews regarding crypto and digital currency accounting matters.

By: Carter Cameron-Huff, CA, CPA, CIA, CRMA

Cryptocurrencies are becoming more mainstream, many companies are now accepting it for payment and willing to do business denominated in it. While many people understand the ins and outs of cryptocurrencies and many business people understand the frameworks for reporting financial information, bridging the gap between these two knowledge sets can be daunting.

This article explores some of the basics of how cryptocurrencies functions as a medium of exchange and what sort of justifications exists for recording transactions. This article is based on current accounting guidance which requires quite a bit of interpretation to apply to a new technology such as cryptocurrency; however with a little time we can arrive at conclusions firmly supported which will provide a good basis for reporting.

This article relies upon guidance given by the Canada Revenue Agency (CRA, similar to the IRS in the USA) and gives direction for applying International Financial Reporting Standards (IFRS), a popular international accounting framework, as well as Accounting Standards for Private Enterprises (ASPE), a popular simplified accounting framework used in Canada.

Recording Expenses

If a company renders payment for a good or service in cryptocurrency (assume Bitcoin (BTC) for simplicity) how should the company making the payment record the transaction in the general ledger?

The general ledger consists of all the accounts a business requires (e.g. sales, rent expense, capital assets) and contains a record of all the individual transaction incurred, the final account balances in the general ledger forms the basis for the creation of financial statements (income statement and balance sheet) as well as the corporate tax return. Recording transactions reliably in the general ledger is important to ensuring financial statements and tax records are a fair presentation of the business.

There is a lack of clear regulatory guidance on the appropriate treatment of cryptocurrencies; however adapting existing guidance for similar transactions can derive a basis for record keeping. The CRA has background statements related to the treatment of cryptocurrencies; based on the CRA's interpretation of BTC, reasonable conclusions on the appropriate treatment under the two most popular Canadian accounting frameworks (Accounting Standards for Private Enterprises (ASPE) and International Financial Reporting Standards (IFRS) which is also popular internationally) can be made.

Finally, the below assessment is for routine business transactions, more complex transactions would need to be assessed on a case by case basis using accounting standards and tax rules.

CRA Interpretation of the Nature of Cryptocurrency

The initial step to ensuring our treatment of BTC will be acceptable to tax authorities and users of financial information is to examine the CRA's interpretation of cryptocurrencies. Starting our journey based on the guidance of Canada's tax authority provides a good foundation to base conclusions on record keeping and will minimize the potential for differences of factual interpretation and surprise tax bills.

The below interpretation was posted by the CRA in 2013, amongst defining cryptocurrencies it includes the below:

Canada Revenue Agency (2015). What you should know about digital currency. Retrieved from https://www.canada.ca/en/revenue-agency/news/newsroom/fact-sheets/fact-sheets-2015/what-you-should-know-about-digital-currency.html

Canada Revenue Agency (2015). What you should know about digital currency. Retrieved from https://www.canada.ca/en/revenue-agency/news/newsroom/fact-sheets/fact-sheets-2015/what-you-should-know-about-digital-currency.html

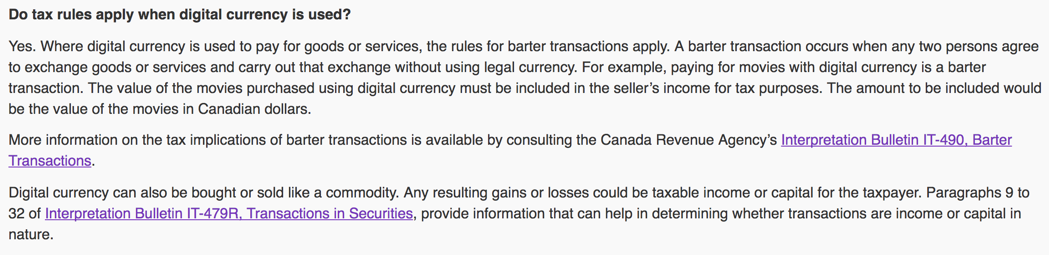

This is confirmation from the CRA that BTC is not treated as a currency and is considered a commodity (like gold or oil), this likely stems from the CRA‘s statement that BTC is not controlled by central banks or any country making it difficult to define it as a currency.

The CRA interpretation states that the rules for barter transactions apply to exchanges involving BTC and therefore any transaction involving it is similar to a trade of non-monetary goods.

Barter Transactions under IFRS

Barter transactions are also known as a non-monetary transaction in accounting terms; this is because no money is changing hands (hence "non-monetary"), one item is simply swapped for another.

Generally in arm's length non-monetary transactions the buyer and seller are exchanging goods with similar market values (or else they wouldn't be trading), that is that the buyer is giving to the seller something of roughly equal value to what they are receiving in substitute for hard currency.

IFRS does not explicitly address non-monetary transactions, but guidance is given for certain types of non-monetary transactions which can be extrapolated to more general transactions.

The clearest statements regarding non-monetary transactions can be found in IFRS section IAS 16 which addresses property, plant and equipment, in accounting terms this means "capital assets", or the assets used to generate the business' income, examples include computers, desks and vehicles.

While not all transactions involving BTC will be for capital assets, IAS 16 provides the strongest guidance on non-monetary transactions and will provide the basis for our conclusions that can be extrapolated to other types of transactions.

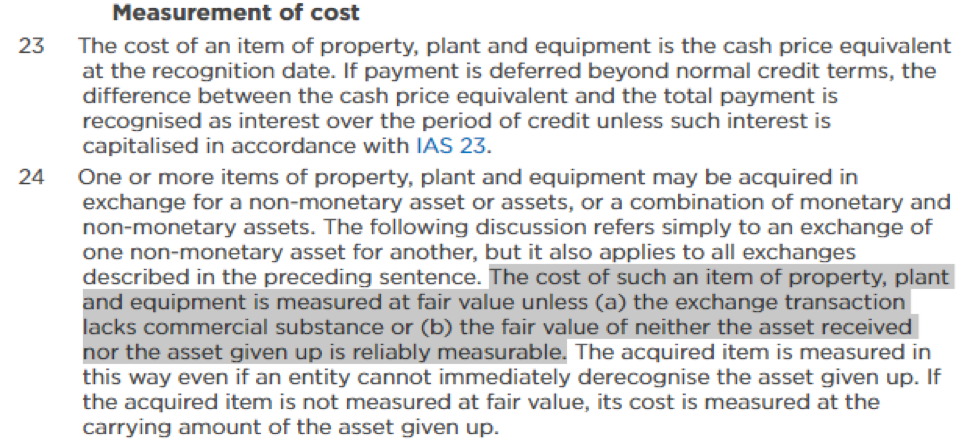

In the Measurement of Cost section subsection .24 we can see the following:

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection.

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection.

Before a transaction can be recorded in the general ledger at fair market value, both criteria a and b must be met. Firstly, that the non-monetary exchange contains commercial substance and secondly that the cost of the item received or given up can be reliably measured.

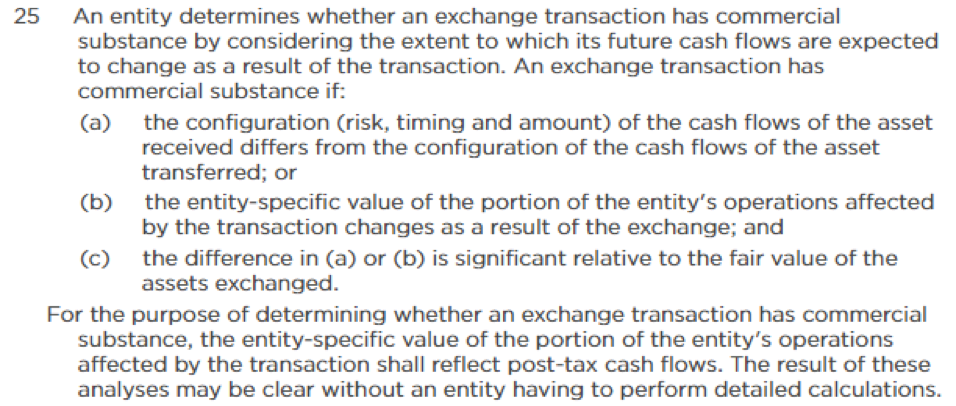

Guidance on the determination of commercial substance is contained in sub-section .25:

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

The first paragraph states that there are two basic requirements, firstly that the amount or configuration of money (cash flow) the business expects to earn differs between that of the asset given up and the asset received.

For example, a computer to be used for the business paid for with BTC has a very different set of anticipated cash-flows (e.g. the money the business generates using the computer) than those of the BTC given up (e.g. the rise and fall of the FMV of the BTC itself).

Alternatively, if the business values the asset received more than the asset given up, the transaction may have commercial substance even if there is no change in the configuration of cash flows. This would depend on the nature of the business and this criterion is included as businesses may exchange for assets with entity-specific value. This guidance is applied specifically for more complex situations.

The second paragraph states that a calculation is not always required to support the assessment of commercial substance; accountants are a reasonable bunch after all.

The guidance for determining commercial substance is primarily an anti-avoidance rule, as long as two parties are dealing at arm's length it is reasonable to assume that in general the transaction will contain commercial substance.

Measurement Basis of the non-monetary exchange under IFRS

Assuming that a transaction contains commercial substance, the guidance per section IAS 16 is that the transaction is to be measured, for accounting purposes, at the more reliably measurable of the fair values of the assets given up (BTC in the example) or the asset received (for instance a computer).

Most assessments of transaction accounting involving BTC gloss over a very unique and key aspect of treating BTC as a non-monetary asset. Generally when exchanging non-monetary assets one of the most difficult aspects is determining the fair market value (FMV) reliably, imagine trading an old pair of hockey skates for a pair of used shoes, the market for these items is fairly shallow so assessing how much each is worth can be subjective.

If determining the value of both the skates and shoes can't be reliably performed, then determining the amount to record the transaction in the general ledger becomes difficult, which means challenging the valuation is comparatively easy for a regulator or tax authority.

BTC mitigates this risk as it is easily measured at any time thanks to a very liquid market. Although the CRA doesn't consider BTC a currency, the reality is that most entities transacting in BTC treat it as an analogue for money, unlike the example of used skates.

As participants in arm's length non-monetary transaction trade like value goods, the goods received for the BTC will have a FMV equal to the FMV of BTC at the time of the exchange. The absence of a disparity in the fair market value of the goods exchanged in a non-monetary transaction eases the record keeping process as well as preventing potential manipulation of financial records through one company recording the exchange at one value and another company determining a separate value.

Therefore there is little opportunity for argument as to what value to record the non-monetary transaction at. For instance if a regulatory body were to argue that the fair market value of BTC at the time of an exchange is the wrong basis of measurement, then the other option per the accounting guidance above is to record the transaction based on the value of the item received in return for the BTC. Due to the free nature of the exchange the item received is going to have the same FMV as BTC, because the contracting parties treat BTC as an analogue to cash.

The implication is that the market price of the BTC at the time of the transaction is the appropriate basis of measurement for the transaction. The timing of the transaction is important due to the volatility of BTC; the timestamp when the BTC is sent is generally a good basis for determining the fair market value.

The date and time of the payment can be correlated with the value of fiat currency in the country the business operates and this serves as an appropriate measure.

Transactions where a business earns revenue by way of Bitcoin are more complicated and outside the scope of this article, furthermore transactions involving a delay between the commitment to send BTC and the actual transfer may involve a gain or loss, which should be recorded.

Barter Transactions under Accounting Standards for Private Enterprises (ASPE)

The accounting treatment under ASPE is very similar in logic to the treatment under IFRS. ASPE is a slightly simplified framework used in Canada while IFRS is an international standard generally implemented in larger or international companies.

Unlike IFRS, ASPE has specific guidance for non-monetary transactions. Section 3831 Non-Monetary Transactions states the following guidance for measurement of non-monetary transactions:

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

For transactions involving BTC the only relevant item is a) as items b) c) and d) are meant to apply to specific circumstances (for example two businesses exchanging inventory assets) and primarily serve an anti-avoidance role.

Similar to IFRS, a determination must first be made as to whether the transaction contains commercial substance; sub- section .11 provides a definition for commercial substance for ASPE:

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

Chartered Professional Accountants of Canada (2017). CPA Canada Standards and Guidance Collection

For part a) it appears that most routine transactions involving the exchange of BTC for goods would meet this criterion, as it is reasonable to assume that the expected cash-flows of the goods received in exchange for the BTC given up will be different.

Part b) will be much less often cited and is generally required in order to account for synergies which might occur when two businesses exchange two assets with comparable cash flows. Consider this specific guidance for less routine situations and meant to guide legitimate non-monetary exchanges where the expected cash flows between the two assets do not differ, but for which the nature of the exchange has bona-fide business function.

Measurement of the non-monetary exchange under ASPE

Assuming that the transaction contains commercial substance, the guidance per Section 3831 is to measure the transaction for accounting purposes at the more reliably measurable of the fair values of the assets given up (BTC) or the assets received (for example, a computer).

Similar to our determination under IFRS, the market price of the BTC at the time of the transaction is the appropriate basis of measurement for the transaction.

Carter Cameron-Huff is a Toronto; Canada based Chartered Accountant (CA), Chartered Professional Accounted (CPA), Certified Internal Auditor (CIA) and holds a Certification in Risk Management Assurance (CRMA). He has experience in the auditing and consulting departments of a large Canadian accounting firm and currently works in banking with a focus on risk and compliance matters. He can be reached at ccameronhuff@gmail.com with any comments or to discuss further any aspect of the article.